Issue:November/December 2017

ONCOLOGY DIAGNOSTICS - Advancements Paving the Way for More Tailored Drugs

INTRODUCTION

Pharmaceutical companies have been subjected to a wide variety of external forces compelling them to get innovative about development of new platforms, liaise with new partners, leverage big data toward precision and predictive diagnosis, and identify new markers. The following describes some of the recent trends observed in the diagnostics industry that are creating opportunities for companies to partner in unconventional ways.

NEW INDUSTRY TRENDS

Liquid Biopsy Attracting Funds From Drug Developers

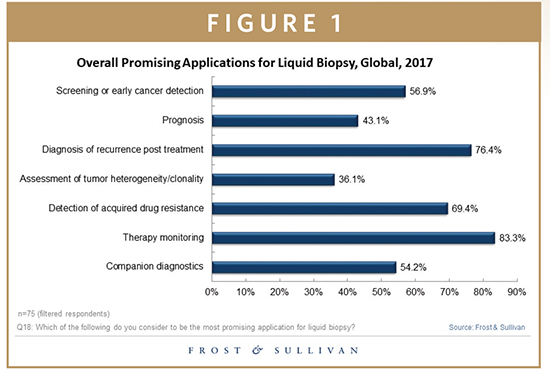

Clinicians have suggested that screening (early detection) and therapy selection, and monitoring are the short-term promising applications of liquid biopsies. Several In Vitro Diagnostics (IVD) and pharmaceutical companies are expanding their product portfolio to include liquid biopsy and companion diagnostic (CDx) in their long-term strategy. Figure 1 shows a Frost & Sullivan survey conducted with almost 100 clinicians is a key indicator of the promising applications of liquid biopsy. There are already a handful of companies marketing tests, but many of its applications are restricted toward improvement of late stage. Investments are flowing into the space where there is potential to develop technologies for early cancer detection and as well as post-cancer monitoring.

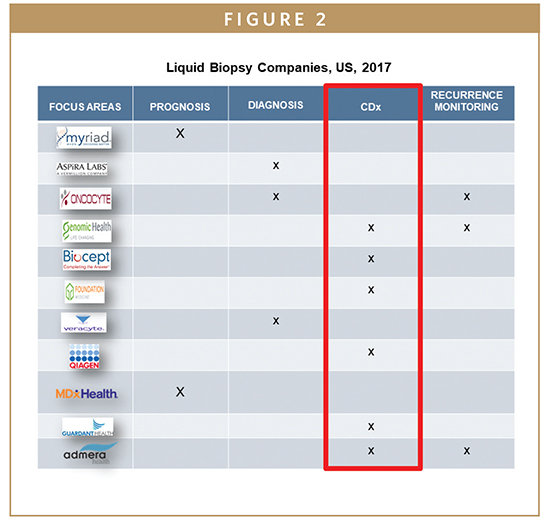

In March 2017, a slew of investors, including Amazon and some prominent pharmaceutical companies like Johnson & Johnson and Bristol Myers Squibb, financed a biotech firm called Grail (a spin-off from Illumina). Grail plans to implement large-scale clinical trials to verify the technology’s ability to detect early stage cancer. Another pharma-diagnostic partnership worth a mention is between BioCept and Catalyst Pharmaceuticals. BioCept’s liquid biopsy tests will be offered to all patients enrolled in its Phase III clinical trial of Firdapse for treatment of Lambert-Eaton myasthenic syndrome(LEMS), a very rare autoimmune disorder. BioCartis and Merck launched their second liquid biopsy test IdyllaTM ctNRAS-BRAF-EGFR S492R Mutation Assay. Some of the other ideal members to partner and to watch over for their CDx portfolio include the companies shown in Figure 2.

Overall, it can be said that technological advances have changed recent sentiments toward circulating tumor cells (CTCs) as valuable predictive or prognostic biomarkers, as evidenced by the growth in comparative studies of genomic mutation analysis in solid tumors and CTCs. Advances such as highly sensitive microfluidic biosensors, single cell analysis, and deep sequencing of circulating cell-free tumor DNA are making the concept of the liquid biopsy, or the ability to monitor a tumor noninvasively, a near-term reality.

Growing Favor of CDx Tests by the FDA

The FDA is going so far as to reject drugs that require CDx for eventual patient selection, such as in the rejection of the Australian company ChemaGenex’s leukemia drug candidate because it did not have a companion diagnostic to select patients. This example signals the FDA’s favorable view of CDx. In December 2016, the FDA also offered an accelerated approval to the first next-generation sequencing–based companion diagnostic test for RubracaTM (rucaparib) developed by FoundationFocus CDxBRCA. Similarly in June 2016, the FDA offered approval to the first-ever liquid biopsy companion diagnostic test from Roche that goes hand in hand with Tarceva developed by Astellas Pharma in the US.

New Clinical Biomarker Classes

Epigenetic regulators are emerging targets for cancer therapy and as future clinical biomarkers. The growing clinical research may lead to novel epigenetic-based companion diagnostics in the future.

Using Big Data From Diagnostic Companies to Tailor Drugs

On March 12, 2015, 23andMe, a consumer genetic testing company announced that it will no longer just sell tests to consumers or genetic data to pharmaceutical companies, but instead, they will start to produce medicine itself. The company has also hired Richard Scheller, who led drug discovery at biotech icon Genentech for 14 years. 23andme has collected DNA information from over 1.2 million people, and it is said the company has sold access to information to over 13 pharmaceutical companies whose names were not revealed except Genentech. This provides evidence that big data can truly revolutionize the pharmaceutical research and development (R&D) industry, as data will help identify new potential drug biomarkers that can be tailored to the genetic make-up of the patient. Based on the big data, patients can be identified for clinical trials with much more ease.

With the ResearchKit, a software framework for apps from Apple, the aim is to collect a myriad of physiological parameters formats, such as blood pressure, heart rate, pulse, between others. A combination of these two datasets both genetic (from 23andMe) and physiological parameters (from Apple) can lead to a breakthrough in analyzing different parameters and provide a 360-degree view to the bits and pieces of data from different corners of the medical research spectrum.

TYPES OF COMPANION DIAGNOSTIC PARTNERSHIPS

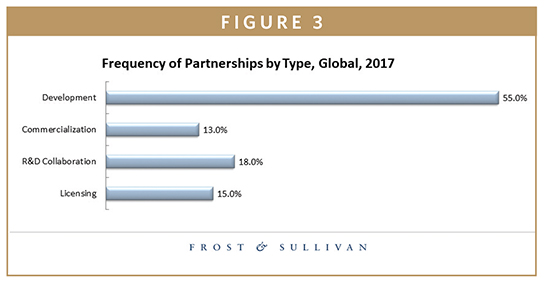

Most pharmaceutical companies developing targeted therapies choose a companion diagnostic partner to access technology and IVD expertise. More than 300 company press releases about CDx relationships from 2011 to 2017 (Figure 3) were analyzed for this research. Partnership types included the following:

-Development: Developing a CDx for a company’s pre-existing drug candidate.

-Licensing: exclusive license between two companies on CDx development and commercialization.

-Commercialization: agreement on Rx-Dx co-commercialization in various market regions.

-R&D Collaboration: permission to use a diagnostic test for drug candidates or funding from the pharmaceutical company for R&D on a CDx.

VARIOUS CO-DEVELOPMENT MODELS EXIST

Approach 1: Leveraging Internal Expertise (eg, Roche and Johnson & Johnson) – The advantages include leveraging existing infrastructure facilitates collaboration and faster release of products. The disadvantages include appropriateness of the diagnostic platform, organizational challenges, and value sharing.

Approach 2: Using an External Diagnostic Partner (eg, Pfizer, Bristol Meyers, Merck, and Amgen) – This is the most common type of partnership and co-development model. This type of partnership provides access to new and appropriate technology through license or fee-for-service arrangement. The disadvantages include negotiating balanced licensing, intellectual property, and partnering agreements.

Approach 3: Acquiring Diagnostic Capability (eg, Eli Lilly, Novartis/Genoptix) – The advantages include access to new technology. The disadvantages include integration challenges between organizations, diagnostic platform may not be appropriate for future compounds.

NEW MARKET OPPORTUNITIES

Critical Unmet Need 1: Even More Clinically Useful CDx Needed to Realize Personalized Medicine

Potential Game Changing Strategy – Biomarker development for future companion diagnostics should incorporate the following functions:

-Patient stratification, eg, a KRAS mutation test to determine eligibility for Eribitux

-Dose determination, eg, CYP2C9 variants to guide Warfarin dosage

-Treatment monitoring, eg, a BCR/ABL PCR analysis that measures response to therapy

-Prognostics, eg, a BRAF mutation test that predicts NSCLC patient survival

CDx developers can follow the above guidance to improve clinical utility.

Critical Unmet Need 2: Unsustainable Drug Development Model

Potential Game Changing Strategy – Biomarker testing in drug development offers the following additional benefits:

-Improving drug efficacy through patient enrichment

-Preventing patient exposure to ineffective medicines and side effects

-Shortening drug development time

-Possibly reducing costs

-Reducing regulatory risk

-Accelerating market adoption of the drug and the speed of commercialization.

CDx developers can convey these benefits to strengthen or increase co-development partnerships with pharmaceutical companies.

Critial Unmet Need 3: Drug Diagnostic Partnerships Are Unfavorable for CDx Developers

Potential Game Changing Strategy – Alternative business models that benefit CDx developers in early partnering deals can include the following:

-Joint R&D investment in CDx development

-Upfront payments from pharmaceutical companies for reaching milestones

-Royalties from future sales

SIGNIFICANCE OF THE CANCER MOONSHOT PROGRAM

Build a National Cancer Data Ecosystem

The objective of the cancer moonshot program is to create a national ecosystem for sharing and analyzing cancer data so that researchers, clinicians, and patients will be able to contribute data, which will be an incentive to invest in artificial intelligence (AI) and data analytics. Companies participating in the working groups are Amazon, Google, Microsoft, and MIT Cancer Center.

Minimize Cancer Treatment’s Debilitating Side Effects

The program also helps with accelerating the development of guidelines for routine monitoring and management of patient-reported symptoms, which will fuel liquid biopsy assay development. Among the institutions participating are the American Cancer Society, Kaiser Foundation Research Institute, UC San Diego Moores Cancer Center, and Louisiana State University.

Expand Use of Proven Cancer Prevention & Early Detection Strategies

Reduce cancer risk and cancer health disparities through approaches in development, testing, and broad adoption of proven prevention strategies will focus investments on screening technologies. Among the companies participating are Huntsman Cancer Institute, Vanderbilt-Ingram Cancer Center, Dana-Farber Cancer Institute, and Janssen Pharmaceutical.

Mine Past Patient Data to Predict Future Patient Outcomes

Predict response to standard treatments through retrospective analysis of patient specimens with AI algorithms. Among the institutions are Oregon Health & Science University, US Department of Veterans Affairs, National Cancer Institute, and Harvard Medical School.

FUTURE OUTLOOK FOR CANCER DIAGNOSTICS MARKET

Changes to Clinical Workflow

Move from disease treatment, to its full potential of preventive medicine. The technology to put Next-Generation Sequencing (NGS) available in every laboratory across the US to the use of improving clinical outcomes for patients and the benefit of their families is available today. We have companies that use a multi-marker approach with ease of use. They provide a panel for 28 of the most utilized gene markers for the high-volume disease. If the physician wants to focus on non-small cell lung cancer or colon cancer then the physician can just use the results for the appropriate gene combinations, usually between one to three markers. The technology allows for mRNA, cell free DNA, and CTC to be measured from blood samples and other body fluids, making it desirable for the screening and monitoring segment. These are the segments of growth in most of the cancers.

Shift in Care From Treatment to Screening

Provide physicians with improved diagnostic accuracy to guide medical decisions in the very early stages of the disease so that the correct therapy can have the effect of suppression therapy and the confidence that their decisions are factual to protect their integrity and that of their practice and hospitals, or healthcare delivery networks by moving the needle from treatment to prevention. For patients and their family with hereditary predisposition to cancer disease, they can undergo regular screening for any signs of early development.

Liquid Biopsy

There is a big limitation in the prognosis and therapy selection segments of the molecular pathology; the space where most companies are today and for which, the FDA has granted approvals for use; the specimen used is biopsies. Biopsies are a surveillance procedure and must be reported centrally and published by the Centers for Disease Control and Prevention (CDC). Physicians and professional medical associations want to decrease the number of annual biopsies. In most of the cancer types, such as colorectal and prostate, the total number of annual biopsies has trended down.

Molecular diagnostics and gene sequencing have proven that with the correct identification of a gene sequence, disease can be identified. But gene expressions are a very complicated science. A single mutated gene can have downstream effects on the activation of another gene or protein expression. The technology is available today for targeting and identifying different markers. Understanding these downstream ramifications and the methodology to measure them will be the proprietary technology for new assays.

Divyaa Ravishankar has over 12 years of experience in market research and management consulting. In addition to authoring numerous reports in the area of In Vitro Diagnostics, she has advised clients on market trends, implications, and strategies on diverse topics as next-generation technologies, end-user and product/feature/pricing analysis, merger and acquisition target analysis, international market expansion strategies, detailed demand modeling, and competitive analysis. Ms. Ravishankar earned her Master’s Degree in Biological Sciences from Birla Institute of Technology.

Total Page Views: 4460